文 | 刘泓君 宋玮

编辑 | 宋玮

经历类似于联合办公独角兽WeWork这样的危机,对软银集团创始人兼首席执行官孙正义(Masayoshi Son)来说,并非是第一次。

2000年互联网顶峰时,孙正义因为投资了雅虎等公司,资产短暂超越微软创始人比尔·盖茨,但他只在首富位子坐了不到三天。随着网络泡沫破裂,软银市值从2000亿美元迅速滑落到20亿,濒临破产。直到三年后才走出泥沼。

一位知名风险投资人告诉《财经》,孙正义的投资方法,几十年其实从没变过。当年VC(Venture Capital,风险投资)投几十万、100万美元,他敢投几千万美元;今天VC可以投几千万甚至上亿美元,他投30亿、50亿美元。软银在WeWork这个项目里就累计花费了近190亿美元。

孙正义打法的核心:一是认知套利,即孙正义常说的时光机理论——充分利用不同国家和行业发展的非平衡。先在发达市场如美国发展业务,然后等时机成熟后再杀入日本,之后进军中国,最后进入印度等;

二是利用非对称性的资金优势来掠取头部项目,头部项目获得巨额资金后继续攻池掠地,进而获取该赛道的垄断地位。

当年对一笔项目投资几千万美元,对全球资本市场不过很小的体量,市场足够消化它的风险。当软银从当年的几十亿美元逐渐壮大到今天Vision Fund(愿景基金)的一千亿美元,当他可以向市场投入一千亿美元,这意味着市场给的估值要达到几万亿。体量之大,超过市场的消化能力。

以WeWork为例,这家声名在外的联合办公概念公司,估值从470亿跌到今天的80亿美元,不是公司自身业务和模式出现了问题,而是二级市场不再认可孙正义给出的高定价。

今天全球资本市场上已经没有人能消化软银所带来的风险——这是软银当前面临危机的本质。

1.Game changer

多数投资人都是Game winner(游戏赢家),而孙正义是少有的Game changer(改变游戏规则的人)。

多年来,孙正义一直的想法是做“全世界最大的企业”。在井上笃夫写的《信仰·孙正义传》的结尾,孙正义说:“位居三流,含恨而死,我讨厌这样的结果。我要成为第一,而且遥遥领先。”

但生于日本、美国求学、日本创业的孙正义或许很早就意识到,自己没有机会通过一个产品或者一个idea从零到一、仅凭实业就做成全世界最强大的企业。

所以他在2019年10月接受《日经商业周刊》采访时发出感叹:“互联网革命发生时,我没能征服。我的确取得了一些小成就,但更大的赢家是Google,亚马逊,苹果和Facebook。与他们相比,我为我们的规模如此之小而感到尴尬。”

1957年出生于生于日本佐贺县鸟栖市的孙正义年少时因为韩国国籍身份在日本受到冷眼,成人时在美国才逐步获得认可,他目睹了日本从强大走向衰落不可逆转的命运,而在美国,他看到了科技加金融的力量可以让一个国家、一个社会、甚至一个个体如此强大。

1981年,孙正义在日本创建软件银行,从一家出版社开始,经过38年的发展,成为了日本最大的网站、最大的电子商务市场和第三大移动通信公司。在海外,软银投资过全球600多家公司,包括给他创造最丰厚回报的雅虎与阿里巴巴。

软银集团今天的市值是773亿美元。但比起孙正义口中的赢家,市值10934亿美元的苹果,这个成绩远没有达到他心目中“全世界最大”的目标。

有一段时间,孙正义曾寄希望与国家合作来创造大型机会。他多次试图让日本、韩国在高速通讯上押上国家的未来。孙正义的一个观点是:“过去三十年,深刻影响了我们的三个指标是:CPU运算能力,存储介质的尺寸和通信速度,这三个指标的增长速度是100万倍。”

1998年6月,亚洲金融危机把韩国推向深渊的边缘,孙正义和他的老朋友比尔盖茨造访了青瓦台。在会谈中,当时的韩国总统金大中问道:“为了重建我们的经济,你认为我们需要做些什么?”

孙正义迅速回应。“有三件事,”他说。“首先,宽带。其次,宽带。第三,宽带。”坐在他旁边的盖茨点点头说:“我百分之百地同意。”

尽管当时金大中并没有完全理解宽带,但这位总统很快就发布了一项行政命令使得宽带覆盖全国。这使得韩国在高速连接方面成为亚洲领先。

2011年前后,孙正义还曾提出过一项雄心勃勃的计划——“亚洲超级电网”,在这一计划下,亚洲的输电线路将提供可再生能源发电——蒙古的风能、印度的太阳和俄罗斯的河流。

孙正义说,“亚洲超级电网”将为所有亚洲国家提供稳定的电力供应。那么,在亚洲范围内采取行动的第一步是什么?孙正义认为,可能是通过俄罗斯港口城市海参崴(Vladivostok)将水力发电从俄罗斯输送到日本,而北海道就在日本狭窄的海上。

因此在2012年夏天,孙正义提出与俄罗斯总统弗拉基米尔·普京(Vladimir Putin)会面的决定。而当时软银的外部董事、优衣库创始人、日本迅销公司会长兼社长柳井正反对这样的私下会谈,他担心孙会因为讨好一名政客而受到公众指责,孙正义的计划告吹了。

对世界经济、政治变化的高度敏锐最终让孙正义抓到了一个大机会,并且他比别人更极致地执行了它。

2016年开始,孙正义组建规模千亿美元的投资基金——“愿景基金”。前百度集团总裁陆奇在接受《财经》采访时称,当时大家都看了这个机会——基金周期会变长、规模会变大。“但孙正义一口气募了一千亿,是让我有点吃惊的。”

创新工场创始人汪华曾告诉《财经》记者,正是因为苹果、谷歌、亚马逊这样超级巨头的出现,使得需要超级大基金来与之抗衡。

“标准的投资只要做好投资就行了,但要和超级巨头抗衡,光做好投资是不够的,更有效的做法是——用足够多的钱,把产业投资和财务投资结合在一起。”汪华说。

作为风险投资人,他们优先考虑的是基金收益,基金规模越大回报率越低,这是一个必然的规律,所以在愿景基金之前,没有人想过可以募集这么一个超大规模的基金——因为它的存在是不合理的。

“而孙正义想的是,他可以通过超大规模的金融资本控制头部公司来实现堪比单一巨型企业对世界的影响力。”一位长期观察软银的投资人说。

孙正义在美国布局、欧洲布局,在中国布局、在东南亚布局,他把世界分为了7个垂直赛道进行投资:消费、企业服务、金融科技、前沿技术、医疗科技、地产建筑、交通物流。他并没有选择向每家公司投资一小笔钱,他更不会在最合适的时候出售股份,以赚取快速的利润。他的做法是:大手笔投资同一赛道的多家竞争公司,谋求大股份甚至控股。

观察孙正义过往的投资组合,他倾向投战争已经结束的公司或者通过烧钱可以迅速使战争结束的公司,因为这样才能保证最大概率压中赛道的最终胜出者。投战争已经结束的公司,最后公司即便最后破产了,孙正义持有的也是债——这又是典型的资本家思路。

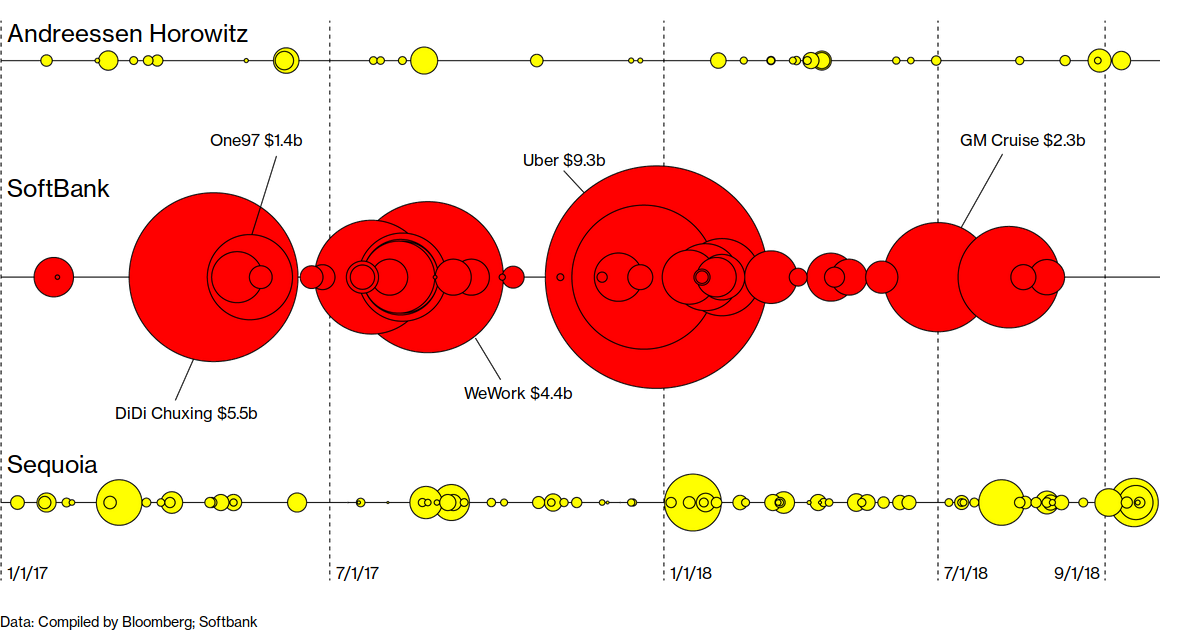

孙正义投资了Uber所有的竞争对手(分别位于美国、中国、印度、巴西和东南亚)并在2018年终于投资了Uber本身,其在UberG轮融资时才入局,一出手就高达77亿美元,一举拿下超过15%的股权,成为Uber占股最大的外部投资者。孙正义甚至一度希望促成Uber和滴滴合并。

“软银不是谁的盟友,而是所有人背后的那只手。”一位创业者评价。

如果每个大赛道通过合并最终形成一到两家超级公司,这些超级公司共同组成一个形成松散的公司网络,而这个网络背后的控制人正是孙正义——这或许是他的终极目标——一个超级网阀建构的终极、有序的世界。

目前,愿景基金在软银集团的地位正变得越来越重要。今年8月,软银在财报展示中,毫不掩饰整个集团“弃实体,转AI投资”的战略倾向。

硅谷老牌风险投资公司Benchmark合伙人比尔·格利(Bill Gurley)将软银的钱比作是“资本武器”。他认为软银的打法在以前的商业史上绝无仅有。这也是为什么,同样是Uber与WeWork的投资方,对软银而言,这两个公司均是软银的“亏损”;但对Benchmark来说,他们成了Benchmark几十倍甚至几百倍回报的新故事。

Benchmark想要的是赚钱,而孙正义,他想要的是传奇。

2. 互联网上半场有效、下半场失效

大约在八九年前,软银的战略团队展开了一项研究,研究集中在一个问题上:为什么在某个时间点以后,英国在赛马比赛中连连惨败?

最后孙正义总结说,英国赛马行业的衰落是由于过分强调纯血统。他认为,赛马和企业都需要新的DNA来发展壮大。

孙正义把找到一个新的DNA比作鲑鱼卵的孵化。雌性鲑鱼一次产的2000到3000个卵中,只有一个雄性和一个雌性卵能够存活下来。如果有更多的存活者,鲑鱼就多到会溢出河流。如果更少,那这个物种就会濒临灭绝。

按照计划,孙正义将投资最多5000家由有前途的企业家领导的企业。这些企业通过联盟或合并来杂交他们的DNA并找到其中幸存的鲑鱼。

我们可以从赛马研究和鲑鱼理论看出一丝孙正义的思考套路:往往从谨慎的研究开始,得出一个非常规但合理的结论,但最终,用一种极端的方法把这个结论运用到现实中。

愿景基金是如何将孙正义的想法付诸实现的?通过采访一些在硅谷的投资人,《财经》梳理了愿景基金的投资套路,它分为“三步”:

第一步,没跟创始人谈之前,孙正义团队研究每个领域最牛的公司,他们花费数月时间了解每家公司和创始人。经过投资经理筛选之后,那些被严格挑选的创业者最后才能参加与孙正义的会面。

第二步,孙正义施展个人魅力的时刻到了。约创始人在自己城堡式的家里聊聊天,或者打打高尔夫,亦或是派出直升机接上创业者。通常聊完5分钟,孙正义会抛出他的经典问题“如果钱不是问题,你会怎么做?”、“我们怎么才能帮助你扩张100倍?”

会面时间基本控制在半个小时之内,出手至少1个亿美元。如果创始人拒绝,孙正义会祭出他的“招牌武器”:“如果你不接受我的投资,我就把钱砸向你的竞争对手。”

有创始人曾经找孙正义融资,本来想融1亿美元,结果孙正义听了五分钟说,我给你7亿美元,但代价是有着高昂的扩张要求。剩下的半个小时都是创始人在砍价,能不能少给一点?

东南亚打车巨头Grab创始人陈炳耀(Anthony Tan)曾经向《彭博商业周刊》回忆几年前孙正义是说服他接受软银投资的情形,孙正义提起了他对马云的早期支持,当时马云是一名默默无闻的教师,现在则始终中国首富。

陈炳耀复述孙正义的话,“多年前,马云就坐在那儿,”孙正义说,“陈炳耀,你收下我的钱。这对你好,也对我好。如果你不要,对你可不太好。

和此前此后的许多人一样,陈炳耀收下了孙正义的钱。同样的故事也发生在了滴滴和Uber身上。

第三步,投完之后,从软银愿景基金会在自己80人的投后管理团队中,派出几位与被投公司一起研究增长策略,并推动被投公司之间的资源整合,甚至业务的扩张、剥离。

软银集团的三步套路显示,孙正义在用PE(Private Equity,私募基金)式的套路去做风险投资。这套投资打法在互联网红利早期是非常有效的,因为互联网红利早期有巨大增长空间,只要赛道选对、头部公司显现,资本便可成为这些公司的战略支点。

但到了互联网下半场,市场进入“L型增长”,这套打法会非常可怕。要把手中募集的巨额资金花出去,孙正义不得不投入那些大赌大赢的公司,但这些公司底盘不稳,软银所给予的巨大投资款又催生了这类创业者+软银自身的盲目自信。这是悲剧的开始。

愿景基金重仓的滴滴、Uber,都是典型的被资本推动长出来的巨兽:不必在业务上竞争,出高价并了就行,将来垄断后能赚回来。

软银的投资鼓励创始人承担过多的风险,但同时,它对创始人只施加了很少的限制,除了不断要求他们扩张、扩张、扩张。一些华尔街的评论者指出,正是WeWork创始人亚当·诺依曼(Adam Neumann)的过度增长策略让公司陷入困境。

孙正义曾说,“公司唯一的上限就是创始人的野心”。他在投资WeWork时告诉诺依曼,“在一场战斗中,疯子比聪明人更容易赢。”

一位跟踪硅谷的记者说,诺依曼创业时还是个“正常人”,但此后越来越失去敬畏心,在被踢出自己一手创建的公司之前,诺依曼沉醉于龙舌兰、大麻、邪教,他把一个CEO能做的“疯狂”事儿都做了。

据《华尔街日报》报道,当诺伊曼准备进行首次公开募股(IPO)时,他正在马尔代夫冲浪,当时纽约的高管们不断请求诺伊曼赶紧回来审阅发布给投资者的重要文件。但诺伊曼不愿缩短行程,而是召集一名WeWork员工到马尔代夫进行现场简报。

软银并没能教育甚至提醒诺依曼如何正确行事。软银是怎么做的?它的做法是,一直试图把WeWork从一家房地产公司包装成一家科技公司、一家AI公司,并高调宣传。

评论家Shira Ovide在Bloomberg的专栏中写到,诺伊曼承受了大部分谴责,但其他人也应该承担责任,比如充斥着重要人物的董事会,包括软银、Benchmark、弘毅资本。

“WeWork不仅仅是某些人的失败,这是过去10年一直处于低息环境的结果,这种环境促使投资人将资金投向那些承诺快速增长的资产。”Shira Ovide写到,“那个愚蠢的时代造就了烧钱的网约车公司、视频公司等等,但那个时代不会永远持续。”

孙正义已经意识到了这一点,他在上个月的一次企业务虚会上告诉企业家,他们需要在几年内将更多的精力放在建立可持续的业务上。同时,他正敦促基金员工推动拥有股份的公司产生现金。

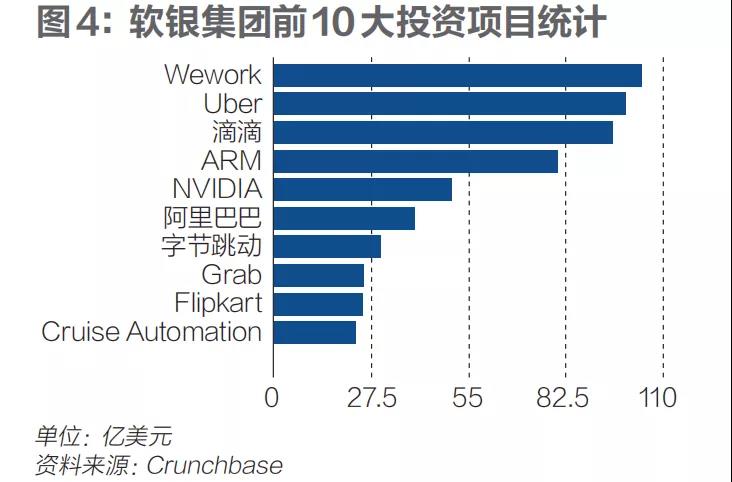

公允地说,软银集团前三大投资项目分别是WeWork、Uber、滴滴,虽然回报率不高,但并不能代表孙正义整体的失败。因为孙正义还投了大量AI和大数据公司、企业服务、医疗科技,这些领域都还没到下半场,还在继续增长。但AI爆发还需要时间,巨大行业集中度的时间还未来临,他们无法消化掉软银巨大的资金。

孙正义的投资方法,必然会碰到经济周期波动带来的挑战。20年前孙正义可以从破产中走出来,核心还是因为他收购了日本雅虎,互联网泡沫破灭后,他又投资了阿里巴巴,这些公司给他带来了顶峰回报,这是优秀公司带来的头部效应。

但今天的问题在于,不管是WeWork还是OYO,它们不是雅虎,更不是阿里;而今天孙正义也没有再遇到当年互联网+移动互联网双浪叠加这样的大机会。

在孙正义身上,可以更深刻看到,每一种投资风格都只能在特定条件下赚一类钱。“绝大部分成功者都一样,就是他的思维方式、资源、特质、timing(时机)匹配了一个时代的大浪潮,浪潮红利结束了,他们也就不灵了。”一位创业者说。

3.谁能阻挡孙正义?

优衣库创始人、日本迅销公司会长兼社长柳井正一直是软银的外部董事。根据日本媒体报道,他至少劝阻过孙正义的一次离职、一次疯狂的扩张想法和一次轻率的承诺。

2016年柳井正曾严厉批评孙正义,因为孙在未经董事会批准下承诺在美国进行大规模投资。当时孙正义向特朗普承诺,软银将在美国投资500亿美元,创造5万个新的就业岗位。

软银集团的董事会有12人,其中包括马云、柳井正在内的四名外部董事,软银董事会的平均年龄是59岁。软银集团没有设AB股,孙正义在软银集团占股21.94%,是软银集团的单一个人大股东,拥有绝对的话语权。

在架构上,愿景基金为软银集团(SoftBank Group)的子公司,除了愿景基金,软银集团旗下还包括了ARM、Sprint、日本雅虎等其他子公司。愿景基金由日本软银集团于2016年发起,2017年成立,是全球最大的私募股权投资基金,规模970亿美元(加上关联基金Delta总额为1030亿美元)。目前,愿景基金财务收入并表到软银集团。

如果说之前软银内部还有人可以阻止孙正义,今天看起来几乎没什么人可以对孙正义说不了。尤其在愿景基金内。

愿景基金的投委会(Investment Committee)只有两个人,分别是孙正义和愿景基金CEO拉吉夫·米斯拉(Rajeev Misra)。换句话说,孙正义不仅不想有不同意见,他甚至可能都懒得听到。

自从三年前成立以来,愿景基金就扩展到了100多名投资人员,并在短短三年内投资了近850亿美元。《财经》了解到,愿景基金在全球有三个最主要的办公室:日本是软银集团所在地,CEO及很多高层将办公室设立在伦敦,美国是愿景基金人数最多的部门,约有400多人。今年开始,伦敦团队正在迅速扩张中,人数已经快接近美国;愿景基金管理合伙人Eric Chen正在上海组建愿景基金中国部,目前扩张到十几个人。

根据《华尔街日报》的报道,愿景基金的许多员工对孙正义做出的投资决定感到沮丧,并且孙与员工的沟通是不畅通的。自今年春季以来,大约有十二名投资人员从愿景基金离职,许多人对缺乏经验的投资主管、团队之间沟通不畅以及激励机制不够感到不满。

愿景基金没有像投资基金一样分享一定比例的投资利润,而是将钱借给员工,让员工将钱共同投资于该基金。这意味着如果基金表现不佳,他们的这笔钱便有去无回了。

在WeWork变成一个烫手山芋之前,软银集团的内部进行过一轮权力斗争,但结局是——那些反对投资WeWork的人都辞职离开。

“WeWork是内部最复杂的案例”,一位软银内部人士告诉《财经》,在后来孙正义对WeWork持续追加的投资中,内部也有很多反对和质疑。

软银的两任前总裁,尼克什·阿罗拉(Nikesh Arora)和阿洛克·萨马(Alok Sama)都是内部对WeWork不看好的人士,他们在投资之前做了大量早期调研,并在2016年就建议不要以80亿美元的估值投资WeWork。

2016年开始,阿罗拉和萨马分别卷入软银内部的股东斗争。有投资者匿名致信要求对阿罗拉进行调查,这个跟孙正义“亲近得有点狂热”的印度人阿罗拉就职不到两年,于2016年中离职。市场猜测阿罗拉的离开与软银发起的内部调查和孙正义不愿意退休有关。

为了平息沙特人对软银内部利益冲突的担忧,萨马后来也被禁止参与愿景基金的工作,在2019年离开软银。内部有一种看法,如今愿景基金CEO拉吉夫·米斯拉(Rajeev Misra)在软银内部的崛起,是以牺牲萨马为代价的。

如今,孙正义的左膀右臂,也是愿景基金的核心决策层是以下两位人士:

负责投资WeWork的人是罗恩·费舍尔(Ron Fisher),这位71岁的老爷爷目前是软银集团副主席,也是愿景基金投资负责人,他跟随孙正义多年,是孙正义最信任的顾问,孙正义做任何重大投资决策,他几乎都在场。

罗恩·费舍尔的投资组合并不多。他名下只有两个投资案例:上一个投资的公司是一家IP授权的体育用品零售商Fanatics,之后就是WeWork。这么多年只有两个投资且在不同的领域,这让WeWork看起来更像是践行孙正义的个人意愿。

另一个核心人物是拉吉夫·米斯拉(Rajeev Misra),57岁,此前在德意志与瑞银工作,他2014年开始加入软银为战略投资部的负责人;2017年成为愿景基金的首席执行官。他是帮助孙正义赢得450亿美元沙特基金背后的人,也是愿景基金“股东运动”权力运作的中心。

孙正义这两位左膀右臂对WeWork充分乐观,费舍尔也进了入WeWork董事会。

曾有媒体报道称,软银内部党派林立,高管们摩拳擦掌争得孙正义的欢心。尽管这些反对者并非主要因WeWork而离开,但随着他们的辞职,孙正义身边越来越缺乏“不同意见”。

一位接近愿景基金的投资人士称,目前孙正义招募的投资人在加入愿景之前,多数已很久不在一线。“他无法招到市场上最好的人才。”

孙正义可以否决基金高管的所有投资决策,而且往往是在最后一分钟的时候。《财经》记者独家了解到,OYO进中国的时候,OYO其他投资人都持反对意见,只有孙正义一个人支持OYO进入中国市场。

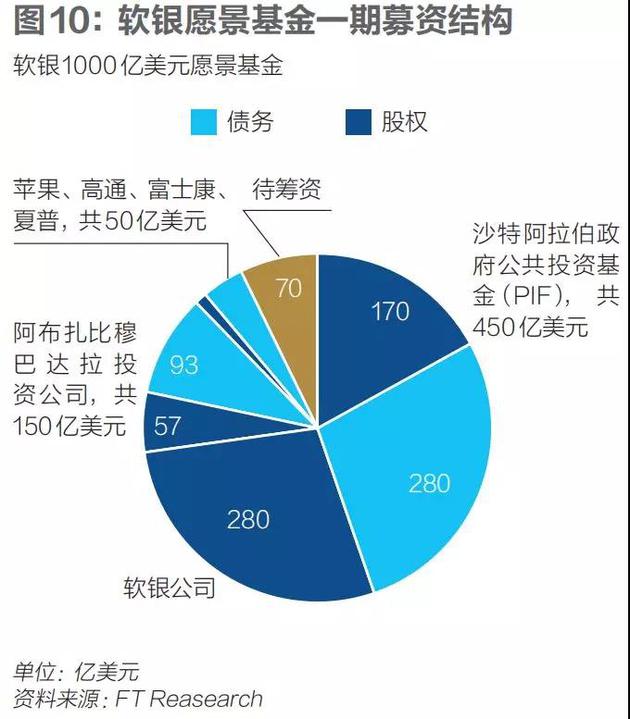

唯一能制衡孙正义的,恐怕只有愿景基金一期最大的LP(Limited Partner,有限合伙人,指出资人)——沙特主权财富基金。愿景基金一期出资人包括沙特公共投资基金(450亿),软银集团(280亿美元),阿布扎比穆巴达拉(150亿美元),以及苹果、夏普、高通、富士康。

沙特保留了他们想否就能否的权利。最初几笔投资时看起来一切都还好,所以沙特没行使这个否决权,由着孙正义一掷千金,直到他们否掉此前软银准备花200亿美元去控股WeWork的豪赌。

但到了正在募集的愿景二期基金时,沙特主权财富基金对二期意愿不大。最后软银集团决定自己投入400亿美元。少了像沙特这样的大LP,投资基金出资人更加多元化,反而加强了孙正义的话语权。

无论是软银集团还是愿景基金,孙正义是绝对的太阳,优点是效率高、目标明确,但内部长期缺乏制衡和反对声音,会让这个组织不够有弹性,让偏执狂更偏执。

从年少时,孙正义就是一位目标至上、厌恶受到他人控制的人。高中时期,孙正义利用暑假期间去美国学习了一个月的外语。回来之后,他只读了一个学期就中途辍学,想转到美国的高中。孙正义当时想要去美国的心情,就如他的偶像坂本龙马脱离土佐藩一样,不顾家人的强烈反对,丢下病重的父亲也要离开。

孙正义深深崇敬坂本龙马(Sakamoto Ryoma)(1836 - 1867),他是推翻德川幕府的关键人物。坂本龙马是胜海周(Katsu Kaishu)的忠实门徒,而这位武士最初打算暗杀后者。

孙曾经对日本媒体表示,他欣赏坂本龙马对待朋友和敌人的方式。然而,孙认为,坂本龙马应该从更广阔的视角看待日本的未来,而不是把一切都看成是黑或白,好或坏。

但对于孙正义来说,好坏不能衡量的东西,盈利或亏损能衡量吗?

4.资本市场已经没人能消化软银

62岁的孙正义以巨大的赌注和对自己信念的坚定信念建立了自己的商业帝国。这种与生俱来的赌徒心态在他第一次遭遇破产危机时就显露无疑。

2000年互联网泡沫破裂,评级机构把软银信用等级定义为BB级“投机型”时,其股价缩水40倍,新资金来源全部断绝,软银陷入绝境。

一年之后,日本宽带政策开放,孙正义决定转型宽带业务“雅虎BB”,他在各个楼道、管道间铺设接线,但遭到日本最大运营商NTT的阻扰。孙正义还需要在最后几栋楼铺设暗光缆就可以连成一个环了,但NTT不愿意交出暗光缆。

面临绝境时,孙正义的解决办法是——去总务省当面抗议,并借来打火机威胁要“自焚”。“你们没什么了不起的,不过是手里有许可权。如果这种状况持续,我的事业也到头了,我会召开记者发布会宣布终止雅虎BB,然后回到这里浇上汽油。”他在现场说。

孙正义在这场旷日持久的战争中斗志高昂,他说自己为了公司可以连命都压上去。在这些困境时刻,孙正义每天工作到凌晨三点,他表现得斗志高昂。

直到2003年,软银还在巨额亏损中。他万不得已出售了青空银行的股份,这是让他最难受的事:“我很害怕,我恨我自己。”直到那一年8月,宽带业务盈利了。软银终于走出泥沼。

过去几十年,软银一直在大起大落中——这极大加强了他的自信。孙正义曾在一片质疑中收购日本掉队的运营商沃达丰,引发股价下跌60%,背负巨债,花了7年时间让它起死回生,成为日本盈利情况最好的运营商。他失手频率一样高,Sprint被收购后一蹶不振,软银债券被调至垃圾级。

今天孙正义愿意花费近190亿美元,寻求一家估值80亿美元公司80%的股份,这不合常理。但这非常像是孙正义做出来的事。如果不这么做,任由几个月后WeWork破产,这起丑闻将会殃及他正在募资的本就不顺利的愿景基金二期;如果这么做,出事也是三年后——那时候,健忘的华尔街和硅谷还能记得起这件事吗?

孙正义20年前的做法和今天的做法没有本质不同,但不同之处在于,以当时软银的体量,市场是有足够空间和时间来消化它的风险。而今天,当他向市场投向了一千亿美元,资本市场上已经没有人能消化它的资金。

一位硅谷的投资人说,他们认为孙正义对未来技术的判断,是违反物理规律的,而这些规律不会因为人的ego大而改变。

孙正义擅长大体量的资本游戏,他能不停从银行贷款、发债,是因为他手里有大量一二级市场的公司股票可以抵押、变现。

但今天的问题不是没有钱,而是钱太多但缺乏有效的行业可以去消化。所以孙正义的问题不会出在钱上,而是处在经济本身的问题上、出在其所重仓押注的行业和公司本身。

关于经济周期的悲观情绪还在蔓延,如果出现任何“黑天鹅”引发这部分质押物的集体缩水,或者软银出现“债务危机”,所有与它相关的科技公司都得跟着遭殃。

要知道,在孙正义募集他的“千亿愿景基金”赚足光环时,软银集团也债台高筑。截止今年上半年,软银有1400亿美元的债务,扣除现金与现金等价物的债务额后,还有460亿美元的净债务。

他曾在2000年投资阿里巴巴2000万美元,2004年投资4000万美元。19年后,孙正义在数次套现后还持有阿里巴巴26%的股票。按照阿里如今的市值计算,仅仅是阿里这部分股票就价值1100多亿美元。

软银曾经通过减持阿里巴巴的股票获取收购ARM缺失的现金流;2019年6月软银还抛售了7300万份阿里巴巴美国存托凭证,占阿里总股份2.8%,成功套现111.2亿美元。

软银还多次在发债时把阿里巴巴的股票作为抵押物——这意味着,一旦软银现金流周转出现问题不得不变卖资产,阿里巴巴也会因股票被抛售一起受影响。同样,如果阿里股价下跌,软银也会面临巨大压力。

阿里的未来和买方市场当然是巨大的,但这些恐怕都装不下孙正义的梦想。

zz 没人买得起孙正义|《财经》

Re: zz 没人买得起孙正义|《财经》

这不就是垄断资本主义的规律吗?但今天的问题不是没有钱,而是钱太多但缺乏有效的行业可以去消化。所以孙正义的问题不会出在钱上,而是处在经济本身的问题上、出在其所重仓押注的行业和公司本身。

此喵已死,有事烧纸

Re: zz 没人买得起孙正义|《财经》

被投资人苦苦哀求少投点,发展不利的解决方案是再多砸点钱。真是疯狂啊。

Re: zz 没人买得起孙正义|《财经》

哇塞! 太#$&* 好看了! 多谢 Knowing!!!

什么是霸权主义,这就是霸权主义啊!

擦亮眼睛,做好爆米花,等着看软银和天朝经济一起落入深谷。。。。哇哈哈哈哈哈

什么是霸权主义,这就是霸权主义啊!

擦亮眼睛,做好爆米花,等着看软银和天朝经济一起落入深谷。。。。哇哈哈哈哈哈

He looked like a small panther, and he moved like a patch of night.

Re: zz 没人买得起孙正义|《财经》

是不是很有豪门阔少把卖唱贫女叫进家唱了个堂会然后让狗腿捧出两套华服一盘首饰逼她做妾的即视感?陈炳耀复述孙正义的话,“多年前,马云就坐在那儿,”孙正义说,“陈炳耀,你收下我的钱。这对你好,也对我好。如果你不要,对你可不太好。

有事找我请发站内消息

Re: zz 没人买得起孙正义|《财经》

活脱脱黑帮模式。从不从?不从就搞死你。会面时间基本控制在半个小时之内,出手至少1个亿美元。如果创始人拒绝,孙正义会祭出他的“招牌武器”:“如果你不接受我的投资,我就把钱砸向你的竞争对手。”

网上搜到原文中的一些图表也挺有意思的。无论是坏血还是 Wework 印度人都有份。再看软银里面的印度人比例。我还是很佩服的。论起骗人和腐败印度人好像比国人段位还要高不少。。。

He looked like a small panther, and he moved like a patch of night.

Re: zz 没人买得起孙正义|《财经》

对对对!我一看到文章里提到孙正义的左右手Mishra来自德银和瑞士银行就脑子里警铃大作!可不就是洗钱高手!

just saw this. lol

I started following pinboard because of the hongkong related news it was tweeting, but turned out it tweets a lot of interesting subjects not just HK.Trying to right the ship is Vision Fund leader Rajeev Misra, a former Deutsche Bank executive who ingratiated himself with SoftBank boss Masayoshi Son by knowing how to find cash when it needed to buy cell phone carriers and controversial bets.

Last edited by april on 2019-11-01 13:45, edited 3 times in total.

He looked like a small panther, and he moved like a patch of night.

Re: zz 没人买得起孙正义|《财经》

This was from last year, have some interesting tidbits, too. not as comprehensive as the one by Caijing.

https://www.bloomberg.com/news/features ... nd=premium

Masayoshi Son, SoftBank, and the $100 Billion Blitz on Sand Hill Road

The Japanese dealmaker says he’ll raise a new $100 billion fund every few years. Silicon Valley’s disruptors are struggling to keep up.

By Sarah McBride , Selina Wang , and Peter Elstrom September 27, 2018, 12:01 AM EDT

Two years ago, Masayoshi Son, chief executive officer of SoftBank, sat in a Gulfstream jet high above the Arabian Gulf, en route to meet with potential investors in a new fund that would invest in technology startups. He was going through his presentation with Rajeev Misra, a key lieutenant, when something stopped him.

One of the slides included the proposed size of the fund: $30 billion. The figure would make the Vision Fund, as Son had named it, about four times the size of the largest venture capital fund ever created and bigger than any private equity fund in history.

Son stared at the number for a moment. Then he deleted the three and replaced it with a one and another zero. “Life’s too short to think small,” he told a stunned Misra.

When Son came to the $100 billion slide in his presentation a few hours later, the prospective investors—executives from a state-owned fund in the Middle East—laughed. Son didn’t, continuing his presentation as if nothing had happened. “He didn’t miss a beat,” recalls Misra, now the fund’s CEO.

SoftBank’s Vision Fund would gather almost $100 billion, including $45 billion from Saudi Arabia’s Public Investment Fund, as well as capital from Apple Inc., the government of Abu Dhabi, and others. “One hundred was a simpler number,” Son says during a September interview at the Tokyo headquarters of SoftBank Group Corp., a sprawling conglomerate that includes an enormous Japanese mobile phone carrier (also called SoftBank), a leading chipmaker (Arm Holdings Plc), and a majority stake in Sprint Corp., the U.S. wireless carrier.

As an investor, Son has been prescient. He was one of the earliest backers of Yahoo! and then teamed up with the dot-com-era darling to launch Yahoo! Japan, a property that wound up being much more valuable than its parent. In 2000 he put about $20 million into Alibaba Group Holding Inc. That stake is now worth roughly $120 billion.

But the Vision Fund is something new: An all-out blitz on the heart of Silicon Valley venture capital, Sand Hill Road. In less than a year since the fund first began making investments, it has already committed $65 billion to acquire big stakes in Uber, WeWork, Slack, and GM Cruise. Son tells Bloomberg Businessweek that he plans to raise a new $100 billion fund every two or three years and will spend around $50 billion a year. For perspective, in 2016, the entire U.S. venture capital industry invested $75.3 billion, according to the National Venture Capital Association.

Outfunded

Size of deals led by three prominent venture capital investors since January 2017

Son’s audaciously large bets have astonished and confused Silicon Valley, where even the most respected venture capitalists have found themselves outmaneuvered by a relative newcomer. The standard VC playbook involves making small, speculative investments in early-stage startups and adding funds in follow-on rounds as those startups grow. SoftBank’s strategy has been to put enormous sums—its smallest deals are $100 million or so, its biggest are in the billions—into the most successful tech startups in a given category. If the local VCs are freaked out by this, the startups seem to love it. SoftBank has given them the equivalent of an all-you-can-eat buffet of foreign investment dollars. “You think they can’t eat anymore,” says Jules Maltz, a partner with IVP, a Sand Hill Road firm. The entrepreneurs “cram it in, put it in their pockets, take doggy bags, whatever.”

The tech industry has seen deep-pocketed outsiders before, but SoftBank is operating at a scale never attempted. That’s driven valuations up, making it difficult for traditional firms to put together enough capital to get into the hottest deals. SoftBank, according to a partner at a major Silicon Valley firm, is “a big stack bully,” a poker term referring to a player with a pile of chips so huge that competitors are afraid to get in the game.

The situation has sent firms scrambling to adapt. Sequoia Capital is raising funds worth $12 billion to stay competitive when bidding on big, late-stage deals. That’s up from about $1.7 billion during a similar period five years ago. Sequoia’s longtime rival, Kleiner Perkins Caufield & Byers, has gone in the other direction, announcing in mid-September that it was breaking up. Four partners, including one of the firm’s stars, Mary Meeker, are leaving Kleiner to start a firm focusing on big bets. The remaining partners will concentrate on earlier, smaller deals. Kleiner’s Ted Schlein has attributed the split in part to a massive amount of capital being invested in startups. He didn’t mention SoftBank by name, but there was little doubt which big stack bully he had in mind.

To most people outside the venture capital industry, Son’s reputation stems less from his big thinking and more from his big spending. In late 2012, shortly after SoftBank announced plans to buy a majority stake in Sprint, Son paid $117.5 million for an enormous Italianate mansion in Woodside, Calif. At the time, it was the most expensive home purchase in U.S. history.

Son says he bought the estate because he doesn’t like hotels and needed a comfortable place to stay when he comes to Silicon Valley. And then, as if to prove that a man with a $117.5 million crash pad can still be a man of the people, he tugs at his gray wool sweater. “I always wear Uniqlo,” he says, referring to the low-cost retailer whose founder sits on SoftBank’s board. Then he lifts his pants leg to show off a stitched brown loafer. “This is a $50 shoe,” he says. Next he pulls at his shirt collar. “This is also Uniqlo. It’s fantastic!”

Son’s upbringing was, in fact, modest. He grew up on the southern Japanese island of Kyushu and was bullied as a child, because his family had come from Korea. Son’s father supported the family through an endless series of ventures that included selling bootleg liquor, raising pigs, and running pachinko parlors. The family adopted a Japanese surname, Yasumoto—a common decision in a country where foreigners face discrimination—but when Son returned to Japan after studying economics at the University of California at Berkeley, he started using his Korean name. “He didn’t want to hide from who he was,” says Hong Lu, Son’s first business partner.

Son founded SoftBank in 1981 as a distributor of PC software. That led to investments in Ziff Davis LLC, the computer trade publisher, and Comdex, the now-defunct trade show in Las Vegas. In 1995, Son wrote a $2 million check during his first meeting with Yahoo co-founder Jerry Yang. He came back a month later offering a $100 million investment, far more than Yang was willing to accept at first. The shock-and-awe offer would become Son’s go-to move.

By 2000, Son had made hundreds of investments and had briefly become the world’s richest man. But then the dot-com bubble burst, and SoftBank lost 93 percent of its market value. A widely reported but apocryphal story says that Son lost $70 billion from his net worth in a single day. In reality it took a little over a year. (He’s now worth $18 billion, according to a Bloomberg analysis.)

Son never stopped making deals. Lu says that Son seemed to be fighting for his life and spent most nights in his office during his post-dot-com scramble. “I thought he was going insane,” Lu says. “He would have meetings at midnight, 3 a.m.” In 2006, Son struck a deal to buy Vodafone Japan and then landed an exclusive deal to distribute the iPhone, which turned around the struggling carrier.

By 2010, Son seemed to be settling into middle age as an opportunistic dealmaker. But he surprised investors that year with a two-hour speech at a shareholders meeting that attempted to articulate a plan for the next 300 years. The rambling 133-slide presentation was chock-full of stock photos and touched on everything from the role of technology in fixing human suffering to why companies fail. Son finally wrapped up by saying he was creating a “strategic synergy group”—an extended family of companies, in which SoftBank would buy stakes of from 20 percent to 40 percent. The companies would have a common mission: “Information revolution—happiness for everyone,” as he put it. Opinion was divided on whether the presentation was an inspiring display of Son’s brilliance, or an amusing demonstration of his kookiness.

The Vision Fund is now run by nine managing partners—five at the fund’s Silicon Valley outpost, two in Japan, and two in London. Son says he personally trained these “hunters” on how to find the best investments and plans to increase the number of dealmakers to 300 over the next few years.

Managing partners filter potential investment ideas and hold a weekly call to discuss progress. Once the prospects are vetted, they go to the investment committee, which is made up of Son, Misra, and a third SoftBank executive, Saleh Romeih. In June, Son said he’d spent 97 percent of his time on SoftBank operations. In his interview with Businessweek, he says that figure is down to 3 percent, with the vast majority of his time spent on dealmaking.

Despite a reputation for throwing money around, Son isn’t an easy mark, his partners say. “If it was a rubber stamp, that would be a lot easier,” says managing partner Jeff Housenbold, former CEO of Shutterfly. “You have to get through the intellectual rigor of convincing him that this is a deal we should do.”

Decisions can take months. When SoftBank began exploring an investment in Uber Technologies Inc. in 2017, the ride-hailing startup was in a state of turmoil, having been the subject of allegations of sexual harassment and other assorted ethical failings. The board had stripped the by-then notorious Travis Kalanick of his CEO duties, and an early investor was suing to kick him off Uber’s board.

Son and Misra faced resistance from Uber, as well as from businesses in their portfolio, which include ride-sharing companies Didi Chuxing in China, Ola Cabs in India, and Grab in Singapore. “We had to persuade people in a big way,” says Misra, who was a senior executive at Deutsche Bank AG and UBS Group AG before joining SoftBank in 2014. He argued that it made more sense to have Uber “in the family rather than not.” SoftBank ultimately invested $7.7 billion in Uber, its biggest single bet to date. The stake is now worth around $11 billion.

Has the SoftBank CEO personally ever taken an Uber? “Yeah,” Son says. “We ordered with my assistant in a European country. I forget which. London, maybe. It was a fantastic service.”

In describing the vision behind the Vision Fund, Son sometimes uses the term gun-senryaku, a Japanese expression that describes the way a flock of birds flies together. His hope, he says, is that portfolio companies will help one another and head off copycats. In Southeast Asia, for instance, SoftBank has encouraged Grab to form joint ventures with a handful of portfolio companies to help those startups break into the region. Grab CEO Anthony Tan is in charge of the effort. Son says similar partnerships are in the works around the world. “You don’t want to go into every little country and try to fight,” Son says, addressing prospective competitors. “You should go there and partner with Grab and the Vision Fund will invest.”

Another portfolio company, Plenty Inc., an indoor farming startup, has been in discussions on a possible collaboration with Katerra Inc., a startup also backed by the Vision Fund that’s working with new technologies to make building construction more efficient, according to Matt Barnard, Plenty’s CEO. Meanwhile, Vision Fund-backed Mapbox has joined with Arm, SoftBank’s U.K.-based chip company, to bring its machine learning software to the billions of devices that use Arm chips, including smartphones and cars.

Entrepreneurs who have taken money from Son cite numerous examples of SoftBank providing help with international expansion. SoftBank’s giant checks also force other VCs to think carefully before funding startups that intend to compete with companies in its portfolio. “We’re seeing more and more cases where the No. 1 company in a particular market is not just a little bit bigger, but actually orders of magnitude bigger, and the Vision Fund is investing in those companies specifically,” says Stewart Butterfield, CEO of Slack Technologies Inc. Butterfield’s company raised $250 million in a round led by the Vision Fund at the end of last year at a valuation of more than $5 billion. Slack, like so many Vision Fund companies, is much larger than its closest competitors. “This is not like established industries—say, automotive—where you had three to four large players, all more or less of similar size and competing at the same level,” Butterfield says.

Son speaking at a news conference in Tokyo on May 9, 2018. PHOTOGRAPHER: NORIKO HAYASHI/BLOOMBERG

SoftBank’s success in pushing fast-growing startups into a dominant position gives Son an advantage when negotiating for a stake in a company. He hasn’t been shy in pressing that advantage. In 2015, online lending startup Social Finance Inc. was looking to raise a few hundred million dollars, but Son wanted to invest more. According to SoFi co-founder Mike Cagney, Son told him that he was going to invest $1 billion in online lending—whether that capital went to SoFi or its competitors was up to Cagney. The entrepreneur opted to take the deal.

Son dismisses complaints from VCs that these tactics are overly aggressive. “They can say whatever they want,” he says. He adds that he has respect for the traditional venture capital business. “I just want to do it my way.”

Hardball tactics aside, others have raised questions about whether SoftBank’s megadeals will be profitable for Son or his backers in the long run. The Vision Fund’s war chest includes about $40 billion in debt, an unusually risky structure for a venture capital firm. Investors have contributed a mix of capital in the form of equity and debt at a 7 percent interest rate. This reduces risk to investors, but it means that SoftBank, which contributed $28 billion in equity, is taking on more risk.

To show a 20 percent internal rate of return on its own capital—which would be a solid return for a VC—SoftBank would need to produce lots of startups with a $10 billion market capitalization and at least two with market caps of over $100 billion, according to research published by EquityZen Inc., a platform for trading stock in privately held companies. That’s a tall order, but Son says delivering high returns should be no problem. He claims that since 2000 his investments—including Yahoo, Alibaba, Vodafone Japan, and the gaming company Supercell Oy—have returned 44 percent annually. For now, investors have bought into his pitch. In late September, SoftBank shares hit their highest level since March 2000, the start of the dot-com crash.

There’s also the question of succession. At one time, Son’s heir apparent was former Google executive Nikesh Arora, but he left two years ago, in part because he worried Son wasn’t going to leave anytime soon. At the time, Son announced that he planned to stay on as CEO of SoftBank for 5 to 10 more years. He compares succession to a relay race, adding that he hopes to turn over the baton to someone who can handle his pace.

“The best batoning is that the guy is running without slowing down, maybe even accelerating at the end,” he says. “And the new guy: rocket start.”

So who’s the new guy? “I don’t know,” says Son. “I will identify within the next eight years.” —With Pavel Alpeyev

He looked like a small panther, and he moved like a patch of night.

Re: zz 没人买得起孙正义|《财经》

这篇太长只看了开头,发现我的一个古老问题得到解答,即雅虎为啥还没破产。生意做大跟经营得好有关系吗?这年头讲什么 meritocracy 是害人吧?

此喵已死,有事烧纸

Re: zz 没人买得起孙正义|《财经》

新听说一个AirTable,投资者其实不懂产品是啥就投资了,现在市值$1bn。莫非又是一个独角兽?

Re: zz 没人买得起孙正义|《财经》

发散一个大家可能不感兴趣的方向,我们最近不是才讨论过小盘股指数表现差吗,很多人认为是过去十年风投大革新, 把本来的未来优质小盘股都养成一统天下的独角兽,预支了上市后的成长红利。

谁道闲情抛掷久?每到春来,惆怅还依旧。

Re: zz 没人买得起孙正义|《财经》

今天f t报道软银在大手笔操作技术股票期权造成纳指狂奔.所有理论猜测解释都错了。看样子未来若干年都透支。传说今天他们爆仓。

https://www.ft.com/content/75587aa6-1f1 ... f866753fa2

https://www.ft.com/content/75587aa6-1f1 ... f866753fa2

谁道闲情抛掷久?每到春来,惆怅还依旧。

Re: zz 没人买得起孙正义|《财经》

I feel like I were living in a fake fantasy world, aka the Matrix. Maybe I am.

此喵已死,有事烧纸